Ep. 18 Krugman on China: No Matter What Happens, He’s Proven Right!

This week’s column is classic Krugman. No matter what happens, he can claim to have predicted it. Or when a country obviously follows his advice, he finds some loophole on which he can blame the ensuing disaster. In this column Krugman discusses the recent plunge in Chinese stock markets, and what if anything it portends for the rest of the world. Finally, a column about economics, at least!

This week’s column is classic Krugman. No matter what happens, he can claim to have predicted it. Or when a country obviously follows his advice, he finds some loophole on which he can blame the ensuing disaster. In this column Krugman discusses the recent plunge in Chinese stock markets, and what if anything it portends for the rest of the world. Finally, a column about economics, at least!

Krugman Column

“When China Stumbles” (January 8, 2016)

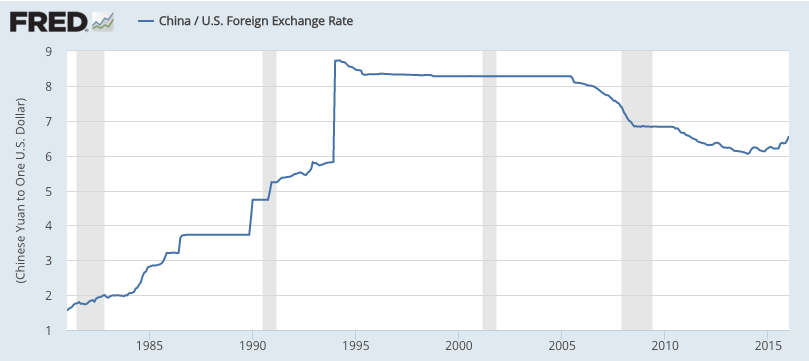

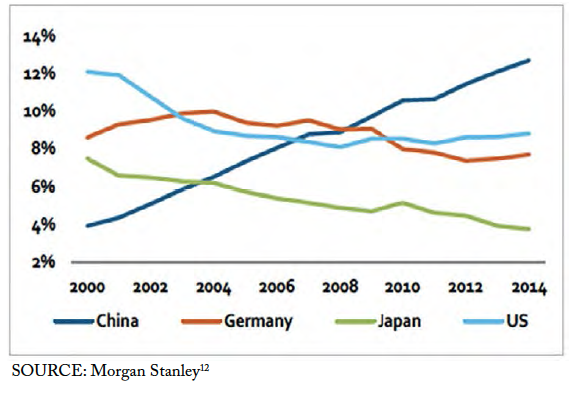

Related Graphics

Special Offers

Get three free issues of the Lara-Murphy Report, Bob Murphy’s financial publication! Click here.

Homeschoolers, no more running yourself ragged: the self-taught Ron Paul Curriculum will give you your time and sanity back, and it’ll give your children an education we would have given a limb for. Plus, get $140 in free bonuses at this link only: RonPaulHomeschool.com.

Need More Episodes?

Check out the Tom Woods Show, which releases a new episode every weekday. Become a smarter libertarian in just 30 minutes a day!